Eli Lilly and Company (NYSE: LLY) was founded almost 150 years ago in 1876 by Colonel Eli Lilly and it is one of the leaders in the healthcare industry. The company has its HQ in Indianapolis, Indiana, has more than 44,000 employees and its products are marketed in approximately 105 countries, as can be seen in their website. They have a growing portfolio of medicines in key areas, which are:

- Alzheimer’s

- Pain;

- Cancer;

- Immunology;

- Diabetes;

- Obesity.

These last two categories are the main reason why the stock is rallying lately, thanks to its new obesity and diabetes drugs Mounjaro and Zepbound. Another factor that is pushing the stock price up, is their new Alzheimer’s drug, which is in late-stage trials.

In 2024, the company had an impressive performance of +45.82% YTD, as shown in the graph down below, that compares LLY performance with the one of the S&P 500. It is believed that the stock has been trading at a premium price compared to its peers, but recently JPMorgan analysts have given to LLY an overweight rating and a price target of $900.

Source: FactSet

We currently have a stake in LLY in our portfolio with an unrealized profit of 46%.

INDUSTRY OUTLOOK

In 2023, the healthcare sector struggled because investors rebalanced their portfolios for a higher interest rate environment. It was a difficult year for companies such as Pfizer and Johnson & Johnson that have seen their revenues being reduced after the lower demand for COVID-19 vaccines. On the other hand, thanks to the surge of GLP-1, Novo Nordisk and Eli Lilly are establishing a dominant position in this sector and are having an important boost of revenues. They are in fact keeping their early mover advantage, even though other companies are now trying to enter this market by experimenting with new formulas both in early and late-stage trials. As reported in the BlackRock global healthcare outlook for 2024, GLP-1 prescription volumes have grown at a CAGR of 45% from 2019 to August 2023, but both the GLP-1 and T2D (type 2 diabetes) have only penetrated 12-17% of the T2D population. This value is expected to grow and, as some companies like Pfizer anticipated, it could double by 2030. But this does not end here. Anti-obesity drugs have the potential to address a population 3 times larger than the one affected by T2D, and at the moment of the BlackRock outlook, only 2% of obese patients were receiving prescription drug treatments. This means that this sector of the healthcare industry has an important growth trajectory for the next few years. According to Morgan Stanley Research, the global market for obesity drugs is expected to reach $105 billion in 2030, up from an earlier forecast of $77 billion.

In regards to the oncology drugs, 2023 was an important year with strategic acquisitions. ADCs have recently been proved to be more efficient than chemotherapy in breast and lung cancer and they only target cancer cells without damaging the normal ones. One of the leaders in this sector is surely AstraZeneca, which has 2 of the 15 ADC drugs approved by the FDA. For this reason, the company has revised its estimates and believes that its revenue in 2030 will be 2 times the one in 2023. In general, not only AstraZeneca sales are expected to double in 2030, but all the sales from the approved ADCs.

Source: BlackRock Institutions

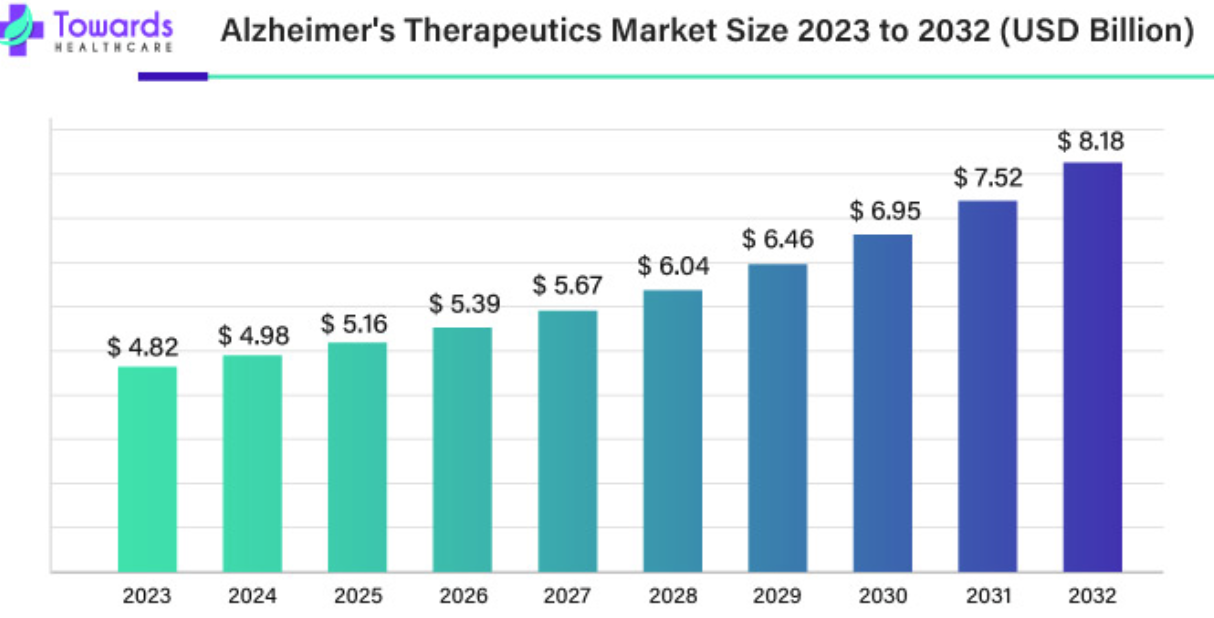

For neurodegenerative diseases, LLY is trying to enter the market already populated by Biogen and Eisai. This sector is very promising and it is expected to reach a market size of $8.18 billion by 2032.

Source: www.towardshealthcare.com

COMPARATIVE ANALYSIS

| Valuation (x) | |||

| Company | Fiscal | EV/ | EV/ |

| Name | Period | EBIT | EBITDA |

| Eli Lilly | 03/31/2024 | 73,31x | 64,42x |

| Johnson & Johnson | 03/31/2024 | 15,84x | 11,98x |

| Pfizer | 03/31/2024 | 121,42x | 25,97x |

| Biogen | 03/31/2024 | 22,43x | 17,18x |

| Novo Nordisk B | 03/31/2024 | 39,89x | 36,38x |

| AstraZeneca | 12/2023 | 29,27x | 19,20x |

| Eisai | 12/31/2023 | 27,46x | 16,47x |

| Average | 47,09x | 27,37x | |

| Median | 29,27x | 19,20x | |

Source: FactSet

As it was said at the beginning, the company is currently trading at a premium price when compared to its competitors, having the second highest Enterprise Value to EBIT and the highest EV/EBITDA.

| P/E (x) | ||||||

| Company | Fiscal | FY1 | ||||

| Name | Period | Date | EV (M) | Actual | FY1 | FY2 |

| Eli Lilly | 03/31/2024 | 12/2024 | 831.719,6 | 127,29x | 62,17x | 44,40x |

| Johnson & Johnson | 03/31/2024 | 12/2024 | 364.399,0 | 21,19x | 13,83x | 13,46x |

| Pfizer | 03/31/2024 | 12/2024 | 216.005,2 | – | 12,17x | 10,48x |

| Biogen | 03/31/2024 | 12/2024 | 38.899,4 | 28,16x | 14,42x | 12,91x |

| Novo Nordisk B | 03/31/2024 | 12/2024 | 637.678,7 | 49,11x | 41,63x | 33,90x |

| AstraZeneca | 12/2023 | 12/2024 | 275.423,8 | 41,55x | 19,64x | 17,06x |

| Eisai | 12/31/2023 | 03/2025 | 11.569,2 | 38,32x | 41,56x | 30,40x |

| Average | 50,94x | 29,35x | 23,23x | |||

| Median | 39,93x | 19,64x | 17,06x |

Source: FactSet

The current and expected P/E ratio does not reassure either, being the highest of its competitors, but it is expected to be 3 times smaller in the next 2 FY.

| Gross Margin (%) | EBITDA Margin (%) | EBIT Margin (%) | Net Margin (%) | ||||||

| Company | Fiscal | ||||||||

| Name | Period | Actual | NTM | Actual | NTM | Actual | NTM | Actual | NTM |

| Eli Lilly | 03/31/2024 | 80,2% | 80,3% | 35,9% | 40,0% | 31,6% | 36,2% | 17,1% | 30,6% |

| Johnson & Johnson | 03/31/2024 | 68,5% | 74,8% | 33,9% | 37,6% | 25,7% | 32,9% | 18,8% | 29,2% |

| Pfizer | 03/31/2024 | 48,9% | 72,1% | 15,1% | 35,8% | 3,2% | 29,6% | -0,5% | 23,4% |

| Biogen | 03/31/2024 | 68,3% | 76,7% | 24,4% | 36,4% | 18,7% | 31,1% | 12,6% | 25,2% |

| Novo Nordisk B | 03/31/2024 | 84,6% | 82,9% | 49,3% | 49,3% | 45,0% | 45,6% | 36,6% | 36,2% |

| AstraZeneca | 12/2023 | 73,9% | 82,5% | 31,3% | 35,8% | 20,5% | 33,3% | 13,0% | 25,4% |

| Eisai | 12/31/2023 | 78,9% | 81,3% | 13,2% | 12,2% | 7,9% | 7,9% | 6,1% | 6,4% |

| Average | 71,9% | 78,7% | 29,0% | 35,3% | 21,8% | 30,9% | 14,8% | 25,2% | |

| Median | 73,9% | 80,3% | 31,3% | 36,4% | 20,5% | 32,9% | 13,0% | 25,4% | |

Source: FactSet

What should reassure investors are surely margins. These margins measure all the company profitability and, the higher they are, the better. These results justify why the company is traded at a premium price, because it is the second best company for these results and is only behind its main competitor Novo Nordisk.

SWOT ANALYSIS

Strenghts:

- Diverse product portfolio, the company produces drugs in several areas, easing off the strong competition that characterizes the healthcare industry. LLY net sales break down by therapeutic fields as follows:

- Endocrinology (57.7%): products for treating osteoporosis, diabetes and growth problems;

- Oncology (19.5%);

- Neurology (8.4%): primary drugs used in treating depression and schizophrenia;

- Other (3,3%).

Source of net sales division: www.marketscreener.com

- Robust research capabilities, Eli Lilly has consistently grown its investment in R&D to maintain its leading position, and now has a broad pipeline of 41 potential new drugs in clinical development and over 20 potential medicines in Phase 3, according to Osum.

- Strong financials and margins, as it can be seen in the table below, the company had an impressive growth in EBIT, which has almost doubled since 2019. The company has too great margins, as reported in the SWOT analysis.

| MAR ’24 | DEC ’23 | DEC ’22 | DEC ’21 | DEC ’20 | DEC ’19 | DEC ’18 | DEC ’17 | DEC ’16 | DEC ’15 | DEC ’14 | CAGR | ||

| LTM | |||||||||||||

| Restate | |||||||||||||

| Sales | 35.932 | 34.124 | 28.541 | 28.318 | 24.540 | 22.320 | 21.493 | 22.871 | 21.222 | 19.959 | 19.616 | 5,66% | |

| Gross Income | 28.803 | 27.042 | 21.912 | 21.006 | 19.057 | 17.598 | 16.812 | 16.801 | 15.567 | 14.922 | 14.683 | 6,32% | |

| EBIT (Operating Income) | 11.346 | 10.325 | 8.280 | 7.548 | 6.850 | 5.790 | 5.785 | 4.931 | 3.871 | 3.592 | 3.329 | 11,79% | |

| EBITDA | 12.912 | 11.853 | 9.803 | 9.096 | 8.174 | 7.022 | 7.394 | 6.499 | 5.368 | 5.020 | 4.708 | 9,61% | |

| Pretax Income | 7.561 | 6.555 | 6.806 | 6.156 | 7.230 | 5.266 | 3.680 | 2.197 | 3.374 | 2.790 | 3.000 | 8,77% | |

| Net Income | 6.138 | 5.240 | 6.245 | 5.582 | 6.194 | 4.638 | 3.151 | -204 | 2.738 | 2.408 | 2.391 | 8,95% |

Source: FactSet

- Reputation and global presence, LLY with its 148 years of history is a worldwide known company which has more than 60% of its net sales in the U.S., almost 20% in Europe, and almost 5% in China and Japan.

- Short interest, the short contracts represent just 0.57% of the outstandings shares. This is a positive factor because just a tiny part of the investors believes that the share price is going to fall.

Weaknesses:

- High dependency on key products, the company is very dependent on its revenue on a small number of products. This might be a problem in the future when for example its patents will expire and new competitors could enter the market, causing a decline in revenue for the company. Also a change of the regulations regarding one of its key products or lawsuits could take a big hit at the company’s revenue.

- Pricing pressures, the industry is subject to pricing pressures, with regulatory bodies demanding price cuts for drugs of primary need.

- Insiders selling, this graph shows only the sales in the last year, and it can be seen that it was quite frequent and particularly during the company’s rallies.

Source: https://www.insiderscreener.com/en/company/eli-lilly-and-co

Opportunities:

- Technology usage in R&D, advancing technology is an opportunity for the company that can use AI in the R&D process to reduce costs and speed up the processes. The usage of AI can also help the company to develop innovative therapies and treatments.

- Aging population, with a longer-living population, there will be a greater demand for pharmaceuticals, especially the ones regarding Alzheimer’s.

- Adverse health occurrences, it is not a very ethical thing to say but situations such as pandemics can boost the company’s revenue.

- Expansion in emerging markets, this could lead to an increased market share and expansion.

Threats:

- Competition, with the expiration of protections on its intellectual property, Eli Lilly & Co. could find itself with new competitors that could result in a loss of market exclusivity and a consequent decline in revenue.

- Changing regulatory landscape, since the pharmaceutical industry is subject to stringent regulatory requirements and pricing pressures, the authorities could reject some pharmaceuticals that LLY is currently developing or, in the case of an economic downturn, the government could set prices for certain drugs, as it has happened with the Inflation Reduction Act of 2022 in the U.S.

WHY DID WE BUY LLY?

Despite knowing that we were buying the stock at a premium price, we decided to buy Eli Lilly at the end of 2023 for its strong market position and because we believed that their new anti-obesity drug could boost its revenues not only in the short-term, but in a long-term perspective. After talking about it internally in the club, and gathering informations, we decided to buy the company because, as I said in the article, there is still a large opportunity of expansion not only in the obesity market, but also in the ADCs, and Alzheimer’s markets.

Author: Filippo Ferrero